Looking for expert guidance on the home buying process? I’ve got you covered! I have put together a comprehensive Free 10 Step Buyer’s Guide that outlines the exact steps you need to take to buy your dream home, and it’s all completely free!

This brochure will guide you through important steps like getting pre-approved for a mortgage, searching for the perfect home, and navigating the negotiation and closing process. It’s like having a personal guide to home buying that fits in your pocket!

To receive your Free 10 Step Buyers Guide, simply provide us with your information and we’ll mail it out to you within 3 business days. Don’t settle for uncertainty when it comes to one of the biggest purchases of your life – get our expert guide and take the first step towards owning your dream home today! This brochure is available for all Kentucky residents. Alternatively, I can hand it to you during our 1st home showing. Either way, fill out the form so I can get your information to serve you better.

The mortgage calculator will help you find out how much you can afford based on your income and estimate monthly mortgage payments. It can also calculate the total interest paid over the life of the loan. As well as determine how much home one can afford based on the income and expenses. Use it to compare different mortgage options and terms. Aso for analyzing the impact of making extra payments or refinancing on the overall mortgage loan.

Mortgage Calculator

You might just like to type in your figures. This one might be more straightforward for you.

Other uses for the above mortgage calculators would be planning a budget for buying a home and managing mortgage expenses. It can be used for understanding the effect of down payment and interest rate on the overall mortgage payment. When you need to consider the affordability and feasibility of different houses and mortgage options, this calculator is also very useful. You can also evaluate the benefits of different loan types, such as fixed-rate mortgages or adjustable-rate mortgages.

Don’t forget to use it to determine whether mortgage insurance is required and how it affects the monthly payment. It is important to compare the costs and benefits of different mortgage lenders and refinancing options, this mortgage calculator will be very handy for that too. You can use it for planning additional expenses such as property taxes and homeowner’s insurance. Lastly, use it for forecasting the impact of changes in interest rates or property value on mortgage payments.

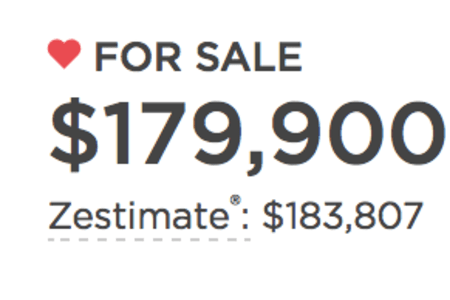

Search properties for sale to see what you can buy

The shortcomings are limitations of online home valuation tools, and it’s important for homeowners to understand these limitations when considering using them. Here are some warnings about the most common limits of online home evaluation tools:

Warning! You Could Lose Money Trusting Online Home Valuation Tools

[rover_idx_home_worth]

Use the above quick home valuation tool to see what I mean. To get an accurate valuation, more information is needed.

1.Home Valuation Tools Only give Estimates:

Online home evaluation tools provide a rough estimate of a home’s value based on publicly available data and algorithms. They do not account for the unique features and characteristics of a home or the local market. As a result, they may provide a less accurate estimate of a home’s value.

2. Home Valuation Tools Lacks personalization:

Online home evaluation tools do not factor in the specific needs or preferences of a seller. They cannot provide personalized recommendations on how to improve a home’s value or how to best sell it.

3. Home Valuation Tools have Limited scope:

Online home evaluation tools only consider data that is publicly available, such as recent sales data, tax assessments, and public records. They cannot account for off-market transactions or other factors that may impact a home’s value, such as neighborhood trends or future development.

4. Home Valuation Tools have Varying algorithms:

Different online home evaluation tools may use different algorithms to calculate a home’s value, meaning that estimates from different tools may vary widely. This can lead to confusion and uncertainty for homeowners.

5. Home Valuation Tools have Legal concerns:

Depending on the state or country, some online home evaluation tools may not be legally allowed to provide home valuations or may be required to include disclaimers about their accuracy. Homeowners should be aware of these legal concerns before using online home evaluation tools.

6. Home Valuation Tools can provide Inaccurate data:

Some online home evaluation tools may use incomplete or outdated public data, which can lead to inaccurate valuations. Additionally, they may not have access to information about recent renovations or upgrades that could positively impact the home’s value.

7. Home Valuation Tools have Limited market insights:

Online home evaluation tools may not consider the nuances of a local real estate market, such as fluctuations in buyer demand or recent changes in zoning laws. This limited view of the market can result in an inaccurate valuation that doesn’t reflect current market trends.

8. Home Valuation Tools are not inspected:

Online home evaluation tools cannot take into account the condition of a home, which is an important factor in determining its value. A home that’s in poor condition, for example, may have a lower value than a similar home that’s been well-maintained.

9. Home Valuation Tools give an Incomplete picture:

An online home valuation tool may not consider specific factors that influence the value of a home, such as the view, the quality of the neighborhood, or the style and age of the home.

10. Home Valuation Tools have Heavy reliance on data:

While data is a key component of assessing a home’s value, online home evaluation tools may rely too heavily on data, without considering the intangible qualities of a home that can influence its value. Things like curb appeal, layout, and natural light are just a few examples of factors that data alone cannot accurately capture.

11. Home Valuation Tools Lack of context:

Online home evaluation tools do not provide context about the assumptions they make when generating a home valuation. For example, an online tool may assume certain market conditions or factors that are not immediately apparent to the user. This lack of context can result in an inaccurate valuation.

12. Home Valuation Tools have Limited flexibility:

Online home evaluation tools may not provide the flexibility to adjust assumptions or input information that could affect a home’s value. This can result in an estimate that does not match the reality of the property or the market.

13. Home Valuation Tools contain Human error:

Online home evaluation tools rely on algorithms and technology to generate a home valuation, and as such, they are subject to the same potential for error as any other technology. Bugs, programming errors, or outdated data can all lead to inaccurate valuations.

14. Home Valuation Tools Lack of transparency:

Some online home evaluation tools may not provide transparent information about the data and assumptions they use to generate a home valuation. This lack of transparency can make it difficult for users to assess the accuracy of the estimate.

15. Home Valuation Tools have No negotiation:

Online home evaluation tools do not factor in the potential for negotiation that may be present in a real estate transaction. This can lead to an overestimation or underestimation of a home’s value, depending on the goals of the buyer and seller.

16. Home Valuation Tools have Limited scope of data:

Online home evaluation tools may only have access to data from a limited number of sources, which can limit the accuracy of the estimate. For example, they may only consider data from recent home sales, without factoring in other local factors that can affect home values, such as new developments, changes in zoning laws, or shifts in the local economy.

17. Home Valuation Tools have Limited local expertise:

Some online home evaluation tools may not have access to local market experts, who can provide insights about the unique factors that influence home values in a specific area or neighborhood. This can limit their ability to provide accurate valuations for certain properties.

18. Home Valuation Tools are No substitute for professional advice:

While online home valuation tools can provide a helpful starting point, they cannot replace the insights and expertise of a professional real estate agent or appraiser. Homeowners who are serious about selling their property should seek out professional advice to ensure they get the best possible price for their home.

19. Home Valuation Tools give Incomplete comparisons:

To estimate the value of a home, online evaluation tools may compare it to other homes that have sold recently in the area. However, these comparisons may not take into account the specific features or characteristics of the home that make it unique. As a result, the estimate may be less accurate than if an appraiser or real estate agent had made the comparison.

20 Home Valuation Tool have Privacy concerns:

Homeowners who rely on online home evaluation tools to estimate the value of their property may be required to provide personal information, such as their name, email address, or phone number. This information may be shared with third-party vendors or used for marketing purposes, which can be a concern for homeowners who value their privacy.

In summary, while online home evaluation tools can be a helpful resource for homeowners who are looking to get an estimate of their home’s value it is important to keep in mind their limitations. Homeowners who want a more accurate valuation or personalized advice on selling their property should consult a professional real estate agent or appraiser. Online home valuation tools can provide quick and easy estimates of a home’s value. Home owners should consider these limitations.

Homeowners should use these tools as a starting point as they explore their options for selling their home, and work with a real estate agent or professional to obtain a more accurate valuation. Overall, while online home evaluation tools can provide a helpful starting point for homeowners who are curious about their home’s value. It should not be relied on as the sole source of information. Homeowners should still seek the advice of a local real estate professional. Real Estate agents can provide a more personalized and accurate estimate of a home’s value based on the unique characteristics of the property and the local market.

Zillow.com, Redfin.com & Realtor.com are popular online Home Valuation Estimators, use with caution & only for General Estimation and understand their limits.

Get a No Obligation Home Evaluation from a Realtor

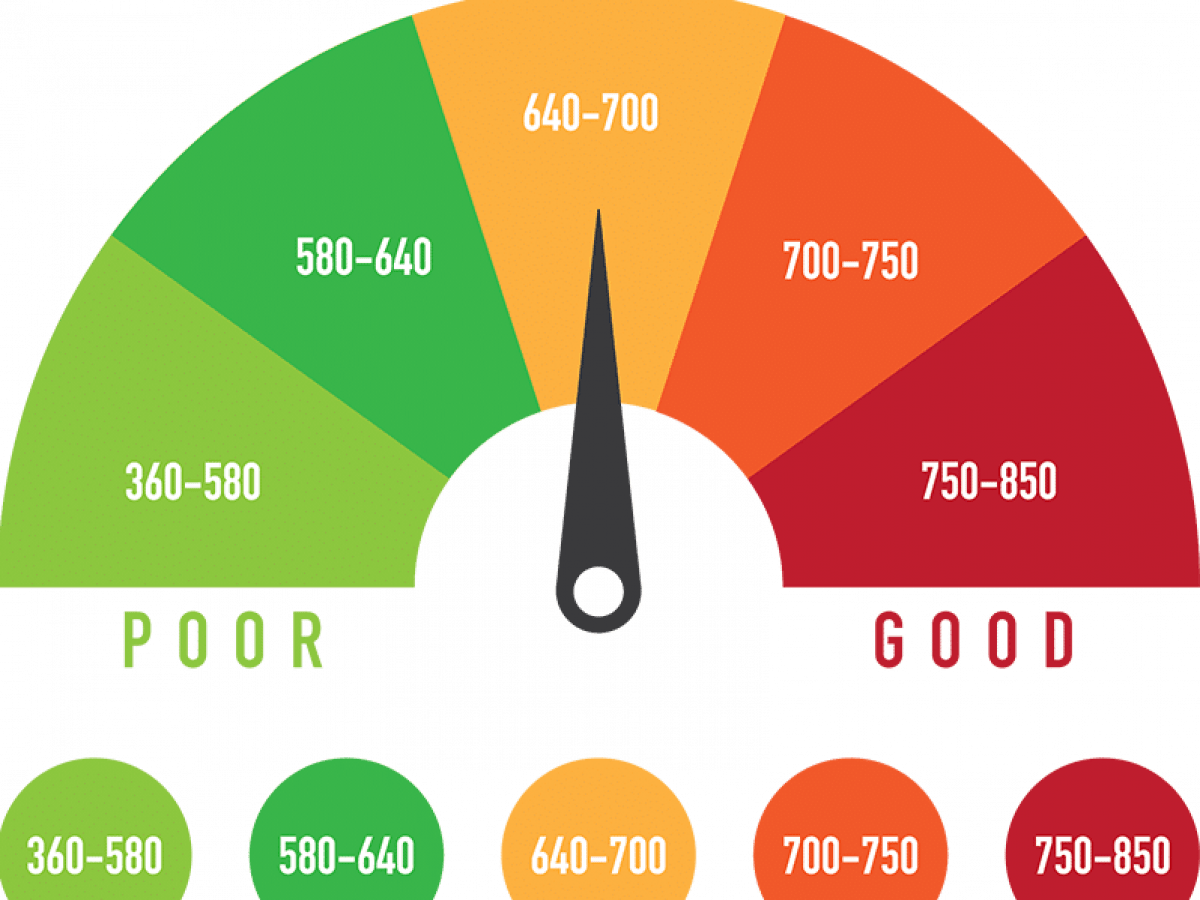

Building good credit takes time and responsible financial habits, but there are ways to build your credit fast. While there are no shortcuts to instantly build credit, there are several steps you can take to establish and improve your creditworthiness over time. Before I tell you the steps to build your credit fast, here are

6 Reasons Why you should build your credit fast

1. Qualify for loans and credit cards:

Building credit increases the chances of getting approved for loans and credit cards when you need them. This includes big-ticket items like a car or a mortgage, or simply small loans and credit cards for everyday purchases.

2. Lower interest rates:

With good credit, you’re more likely to get approved for loans or credit cards with lower interest rates. This can save you money over time by reducing the amount of interest you pay on your debts.

3. Rental applications:

Building credit can make it easier to sign a lease for an apartment or rental home. Many landlords will check your credit history as part of the rental application process.

4. Employment:

Some employers may check credit history as part of the job application process, especially for positions that involve financial responsibilities.

5. Insurance rates:

Credit scores can be a factor in determining insurance rates for home, auto, and other types of insurance. Building good credit can help you receive lower insurance premiums.

6. Improve financial security:

Ultimately, building credit is about establishing financial stability. By demonstrating responsible credit use over time, you can build a solid credit rating that will help you navigate life’s ups and downs, from unexpected expenses and emergencies to planning for a secure financial future.

Here are some strategies to help you build good credit relatively quickly:

1. Obtain a secured credit card:

If you have limited or no credit history, getting a secured credit card can be a good starting point. Secured cards require a cash deposit as collateral, which becomes your credit limit. Make regular, on-time payments, and keep your credit utilization low (below 30% of your credit limit) to boost your credit score.

2. Make timely payments:

Pay all your bills, including credit cards, loans, and utilities, on time. Payment history is a crucial factor in determining your credit score. Late or missed payments can have a significant negative impact on your creditworthiness.

Set a reminder to pay your bills or set your payments to autopay.

3. Keep credit utilization low:

Credit utilization refers to the percentage of your available credit that you’re using. Aim to keep it below 30% to demonstrate responsible credit management.

For example, if your credit card has a $1,000 limit, try to keep your balance below $300.

4. Diversify your credit mix:

Having a mix of different types of credit, such as credit cards, loans, and a mortgage, can positively impact your credit score. However, only take on credit that you need and can manage responsibly.

5. Become an authorized user:

If a family member or friend with good credit is willing to add you as an authorized user on their credit card, it can help you build credit. The account’s positive payment history and age can be reflected on your credit report, but make sure the primary cardholder maintains responsible credit habits.

6. Monitor your credit report:

Regularly check your credit report for errors or discrepancies that could negatively impact your credit score. You’re entitled to a free credit report from each of the major credit bureaus (Equifax, Experian, and TransUnion) once a year.

Try Credit Karma – its free and they will tell you your credit usuage and monitor your payments

7. Avoid excessive credit applications:

Each time you apply for credit, a hard inquiry is placed on your credit report, which can temporarily lower your score. Apply for credit only when necessary and be selective about the applications you submit.

8. Be patient and consistent:

Building good credit takes time and requires consistent, responsible financial behavior. Focus on maintaining positive credit habits over the long term, and your credit score will gradually improve. The longer your history is with good credit the higher your score becomes.

Remember, building credit is a gradual process, and there are no quick fixes. Be cautious of any services or claims that promise to rapidly repair or rebuild your credit, as they often engage in unethical practices and may be scams. Building your credit now will help you get pre-approved for a house when the time is right and your finances are in order.

There are 8 types of home buyers you could possibly be, after you are pre-approved of course. Which one are you?

First Home Buyers: …

The Downsizers: …

The Up-Sizers: …

Luxury Lovers: …

The Investor: …

Long Gamers: …

The Fixers and Flippers: …

Young & Tech-Savvy Millennials:

Knowing the kind of property you are looking for helps me help you narrow down your search. Sometimes there are off the market listings which only get seen by investors or serious buyers. These properties may not even hit the MLS because they are such a good deal or the seller wants to close fast. If you are truly looking for a deal and you are ready to buy, don’t delay. Subscribe to Buyer Alerts below … and/or make sure to click on one of the above Type of Buyers to get more information.

Stopping foreclosure without paying past due money can be challenging, as it typically involves addressing the underlying financial issues. However, here are a few steps you can take to try and avoid foreclosure:

1. Contact your lender:

As soon as you realize you’re at risk of foreclosure, reach out to your lender or loan servicer. Explain your situation and express your willingness to resolve the issue. Some lenders may be open to alternative solutions, such as…

loan modification,

forbearance, or

a repayment plan.

2. Explore loan modification options:

In some cases, lenders may be willing to modify the terms of your loan to make it more affordable. Loan modifications can involve adjusting the interest rate, extending the loan term, or adding the past due amount to the end of the loan. Work with your lender to assess if you qualify for any loan modification programs.

3. Seek assistance from housing counseling agencies:

HUD-approved housing counseling agencies provide free or low-cost counseling services to homeowners facing foreclosure. These agencies can help you understand your options, negotiate with your lender, and develop a plan to avoid foreclosure. They may also assist in working out a repayment plan or connecting you with local resources.

4. Consider a forbearance agreement:

If your financial hardship is temporary, you may be eligible for a forbearance agreement. This allows you to temporarily pause or reduce your mortgage payments for a specific period. However, it’s important to note that you’ll still need to repay the past due amount after the forbearance period ends.

5. Sell the property:

List your house for sale. Call (502) 417-3463 and I can give you a Free Home Evaluation and help you sell your house for top dollar. If you’re unable to afford the mortgage payments and it’s not possible to work out a solution with your lender, selling the property could be an option. Selling the home can help you pay off the mortgage and potentially avoid foreclosure.You may need to act quickly and price the property competitively to attract potential buyers.

MORE OPTIONS…

6. Sell Cash to an Real Estate Investor:

If You Need To Stop Foreclosure, I am in contact with many investors who can Buy Your Houses Fast in Cash! Why ask just one investor when you can get more than one offer? Get a fair, no risk offer on your home by Simply completing the short form on this page and I will contact you with investors who are ready to make an offer.

6. Investigate government assistance programs:

There may be government programs available that provide financial assistance or foreclosure prevention options. Research programs offered by federal, state, or local agencies that are designed to help homeowners facing foreclosure. These programs can vary depending on your location and eligibility criteria.

7. Consult with an attorney:

If you’re facing foreclosure, it can be beneficial to consult with a foreclosure defense attorney who specializes in real estate law. They can review your situation, assess legal options available to you, and provide guidance on how to protect your rights and interests.

Remember, the specific options available to you will depend on your individual circumstances, the type of mortgage you have, and your lender’s policies. It’s crucial to act quickly, communicate with your lender, and explore all possible avenues to stop foreclosure. I am here to help guide you if you have any questions concerning any of these options. Don’t feel like you can’t reach out. I want build relationships and help sellers who stuck between a rock and a hard place.

2.

2.  3.

3.  4.

4.  5.

5.  6.

6.  7.

7.  8.

8.  9.

9.  10.

10.  11.

11.  12.

12.  13.

13.  14.

14.  15.

15.  16.

16.  17.

17.  18.

18.  19.

19.  20 Home Valuation Tool have Privacy concerns:

20 Home Valuation Tool have Privacy concerns:

6 Reasons Why you should build your credit fast

6 Reasons Why you should build your credit fast

List your house for sale. Call (502) 417-3463 and I can give you a

List your house for sale. Call (502) 417-3463 and I can give you a